Current users

Sign In

New users

Join Today

Posted: 08/30/2019

Posted: 08/30/2019

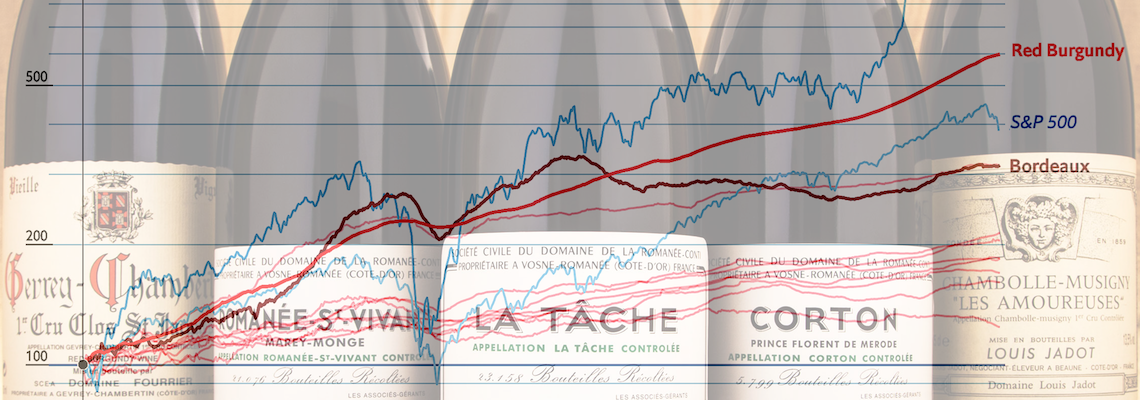

Last week, The Economist magazine's Data Editor, Dan Rosenheck, leveraged a 16-year data sample from WineBid to publish an article stating Burgundy Wine Investors Have Beaten the Stock Market. The Economist concluded that Burgundy wine has beaten the S&P 500 by nearly 200%, if an investor had invested in both back in 2003. The article further suggests that Bordeaux, Champagne, California and other regional wines (Italy, Spain, Rhone, Australia) were not as good investments over that time period (with no comment about forward-looking investability). Additional statistics describe how wines highly scored by wine critics, especially those over 90 and even further after 96, appear to have greater appreciation.

Following the publication, various wine aficionados, economists, and data-geeks on Twitter and WineBerserkers, among other communities, had a great time debating the conclusions. As the provider of the data and as the largest and longest-standing online wine auction in the world, we at WineBid thought to provide a few more insights as fodder for the great “wine as an investment” debate.

First and foremost, we believe that wine is much better collected, consumed and shared with friends than actively traded. We do not claim to be investment advisors, economists, or commodities traders. WineBid is a global online auction platform that provides a buying and selling marketplace with the most real-time actual trade data, authentication, and fulfillment systems for consignors and buyers. That said, there are definitely individuals and companies who make money trading wine on their own account, either with a Warren Buffet style “buy and hold for the long term” approach, or as modern day-traders looking for arbitrage opportunities across markets, channels and individual bottles of wine.

The analysis and follow-on comments below are meant to be interesting rhetorical thought pieces for a broader audience, not advice on investments or wine trading. These are again meant to stimulate thought around how wine, which has both primary and secondary tradeable and trackable markets, can be considered an alternative asset class to be compared against stocks and other investable assets.

Here are some of the reasons we see individuals looking at wine as an interesting alternative asset class:

• Some wines are known to appreciate: As the Economist article points out, some regional indices of wine appreciated significantly in value over the 16-year time period (although the author also points out there are time slices when prices depreciated as well). Very specific individual bottles by certain producers of certain vintages have made spectacular headlines. Many people were enthralled when two bottles of DRC sold earlier this year for nearly $500K each. First Growth Bordeaux, Grand Cru Burgundies, and California Cult Cabernets are the wines thought of as the most collectible and tradeable over time.

• Supply seems constrained and dwindling while demand grows: There is a finite amount of production of First Growth Bordeaux and Grand Cru Burgundy each year. As each vintage ages, some of what was produced gets consumed, and some pass their peak drinking window. This leaves less supply of older great vintages, with a highly variable and imprecise “expiration date.” Meanwhile the global population of wine appreciators is growing, with broader demographics and more online access and information, creating heightened international demand for 24/7/365 instant gratification.

• Significant amounts of data exist for pricing and other factors: Individuals who like to trade and collect - whether investments, baseball cards, vintage cars, or wine - always value assets and markets where data is ample to abundant, which they use to create their own unique angles for investment and “alpha” for premium returns. WineBid has the one of the most comprehensive, accurate and up-to-date databases available with over 20 years of trading history, much of it easily available on the site with various forms of trading data at the aggregate and lot level. Additionally, there are several other outlets who provide various forms of more limited data sets (mostly behind paywalls), and other useful data like production data, weather data, critic scores, and community scores from which to create various possible predictions on pricing.

• There is a reasonably liquid secondary market in wine: While not as liquid as the stock market or bond market, the presence and frequency of secondary markets in online auctions like WineBid, and the oldest offline wine auctions such as old brick and mortar houses like Sotheby’s, make wine a more plausible asset to think about for trading and investing.

All of these attributes make wine an attractive and tempting candidate to consider for investment. With this in mind, the Economist laid out (and we will highlight and extend) many critical factors when considering it as such. This is not investment advice. WineBid highly recommends wine be purchased for enjoyment, first and foremost. But for would-be wine investors, here are key highlights to consider:

• Wine market conditions significantly impact absolute returns versus other market conditions: The article focuses on 2003 to present, as that was the longest time stretch of the data provided for the largest data set. In fact, if a reader uses the sliding date scale provided by the Economist, at certain points like July of 2018, both Bordeaux and Burgundy outperform the S&P 500 to present. Just like with any investment, market conditions at the time, or entry or exit, can make a big difference in relative returns, particularly in two different asset classes impacted by different factors. The old adage, “Buy low and sell high,” applies as much to wine as to any investment, and knowing where you are in the cycle counts. As the article shows, different regions have different trends in popularity, so knowing what’s trending in which direction is critical, as either a buyer or a seller.

• Wine and other asset classes should be examined for beta for relative returns. The Economist analysis certainly showed, at some points, that the wine indices seem to track the S&P, which begs the question to what extent they are correlated. Would-be wine investors should consider the degree to which the S&P and other stock prices are more impacted by election years, interest rates, regulatory changes, trade wars, and industry trends, whereas wine prices might be more impacted by weather patterns, production quantity, and changing global consumer tastes. For example, how much is the Asian market continuing to favor Bordeaux, and, more recently, adding Burgundies to the purchase pattern?

• Individual high critic score and well-branded wines have outperformed the indices: The Economist analysis uses a large portfolio of fine wines to create aggregate regional wine indices. Wine buyers tend to buy by the case or the bottle, not by a full regional portfolio. As any investor in general market or sector-specific ETFs or mutual funds knows, individual stocks within a fund can far outperform or underperform its own index, and the market in general, often based on news or brand perception. As the Economist article points out, professionally reviewed wines with critics scores over 90, especially scores over 96 and 100 point wines, show a statistical propensity to appreciate more than lower scored or unscored wines, but the question is cause vs effect. Similarly, individual wine producers and vintages can far outperform or underperform their regional index. Well-pedigreed producers like Lafite Rothschild, Domaine de la Romanee Conti, and Screaming Eagle (which generally also have great critic scores) have been seen to appreciate more than lesser known brands, but being better known, have more efficient pricing and are also generally more costly to procure.

• For risk/return and yield, wine might be better analyzed against Treasuries or gold, rather than equities: The article analyzes wine performance vs the S&P 500, but does not review wine appreciation versus US Treasuries, wine versus gold, or wine versus commodity futures like pork bellies or live cattle futures, which all have their own unique risk/return and yield characteristics. In fact, the long term yield for US Treasuries (especially now with our flat to inverted yield curve) has been between 2-4% over time, even dating back to 2003. Thus, statistically, most regions’ fine wine has appreciated and returned more than than 10 or 20 year bonds held over time, although bond trades have actually been up recently, given global economic conditions. Similarly, gold was down significantly over the past 5-7 years, until recent conditions spiked interest in gold as a safe haven again. Each of these asset classes also has unique yield characteristics. Some stocks and funds pay dividends that can be reinvested; some are only for capital appreciation; bonds pay coupons until redemption for face value; gold doesn’t pay dividends, doesn’t expire, and isn’t very consumable. Thus, while looking at wine versus the S&P 500 is intriguing, so is thinking about returns relative to other asset classes as well.

• Fine wines are not as fungible a commodity like other deliverable or non-deliverable commodities and futures: Speaking of commodities futures like gold, feeder cattle or brent crude, it is important to consider that among buyers and sellers of fine wine, provenance is of critical pricing importance, as is actual delivery. Authentication, knowing where a specific bottle of wine was purchased and how it was stored, and the cork, capsule, label and appearance conditions can have significant pricing impacts on individual bottles, which are for the most part, delivered. Conversely, gold, feeder cattle and brent crude futures are generally traded on a homogenized standard of deliverability, and for the most part, delivery is not taken and settlements are made in cash. This article provides a good high level overview of the storage and transportation impact on various commodities, and this second academic paper is an a intensive study on the impact of storage costs on futures pricing in brent crude oil. These factors were not examined closely in the Economist article and would need to be taken into account by any would-be wine traders.

• For wine investment or trading, seek to minimize transaction and storage fees. Transaction costs for stocks and bonds are much lower than for vintage wine for the average trader. Stocks and bond trades are nearly free at many online brokerages, or go up to 1% management fees for high end services firms. Wine pricing at retail is not transparent, with markups of 35% or more. Most auctions have very transparent pricing, and charge a 20-25%+ buyer’s premium. WineBid - at 17% - offers some of the lowest rates for buyers in the business. Thus, the channel of purchase and frequency of trading can make a big difference in net returns. Similarly, long-term storage can be an unfactored cost. Personal cellars require construction, temperature and humidity control and maintenance. Wine storage facilities advertise rates such as “lockers at $80 a month for up to 12 cases” or “$2.10/case for up to 500 cases.” In a surface analysis, it appears that wine can be stored for $0.10-$1.00/bottle/month, assuming 100% utilization of the lockers or storage area provided. Wine storage facilities know, like gym memberships, that clients rarely maximize their utilization. At only partial utilization, an investment-minded individual might want to assume a $0.25-$0.50 cost per bottle per month for storage. WineBid provides a list of great wine storage companies around the country that offer competitive rates. WineBid also offers long-term storage to customers at its warehouse in Napa, CA, at a very competitive $0.25/bottle/month for WineBid Pro customers.

In conclusion, we don’t know if there is a “Warren Buffet of Wine” who consistently beats all major indices. We do know that there are some individuals who are able to buy, store, and eventually consign wine and make some profit from it, or at least intelligently offset their consumption costs.

We will continue to make various analyses available for discussion and debate here on our Wine Auction News blog. As stated earlier, we at WineBid believe that wine is much better collected for personal enjoyment, consumed and shared with others. As an investment, wine should probably be thought of more like Treasuries or gold, with a “buy and hold” strategy, rather than frequent trading, due to transaction costs. If nothing else, long-term collectors can rest assured that thoughtfully purchased and collected wines retain a good amount of value and there’s always a great and liquid market for resale.

Wine collectors thinking of selling their wine can contact us at (888) 638-8968 or easily submit a wine appraisal request here. We do require a minimum appraisal value of $2,500.